State of the Restoration Industry in 2021

The Impact of COVID-19, Today’s TPA Landscape, Restoration Challenges and More

Read the report here.

The purpose of research is to advance our knowledge in any given field of study. As the restoration industry constantly evolves and changes based on the economy, natural disasters, the insurance market, technology, and other factors, frequent research helps identify common behaviors, trends, and beliefs industry-wide.

In May, Restoration & Remediation completed its latest State of the Industry report with the intention of learning:

- Which tools, equipment, and chemicals are currently being used, and future plans for purchase.

- What attributes are important to restoration and remediation contractors when making purchasing decisions.

- The main revenue streams for restoration and remediation professionals, and any expected changes.

- How restoration companies allocate their budgets across equipment, chemicals, technology, and other purchases.

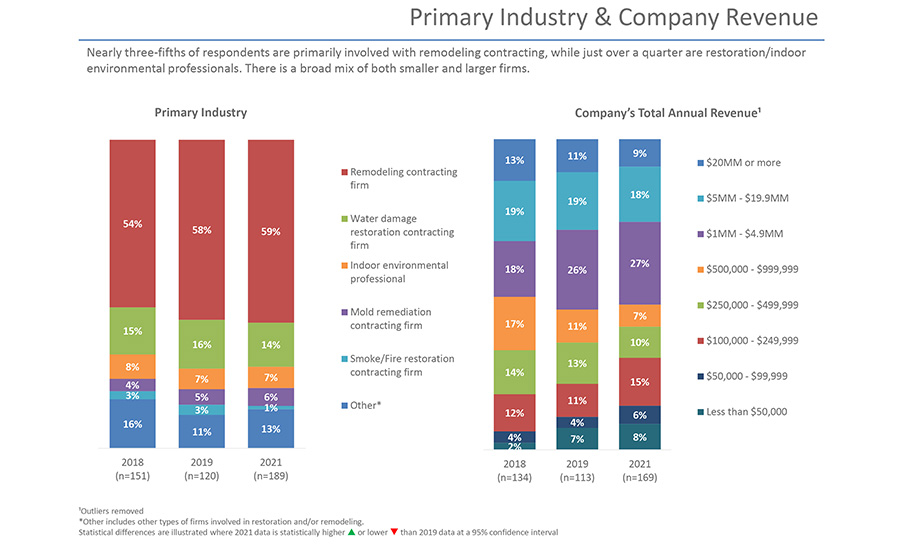

Basic Demographics

Thousands of surveys were sent out; you can see a breakdown of the demographics here, as well as the amount of revenue achieved by respondents.

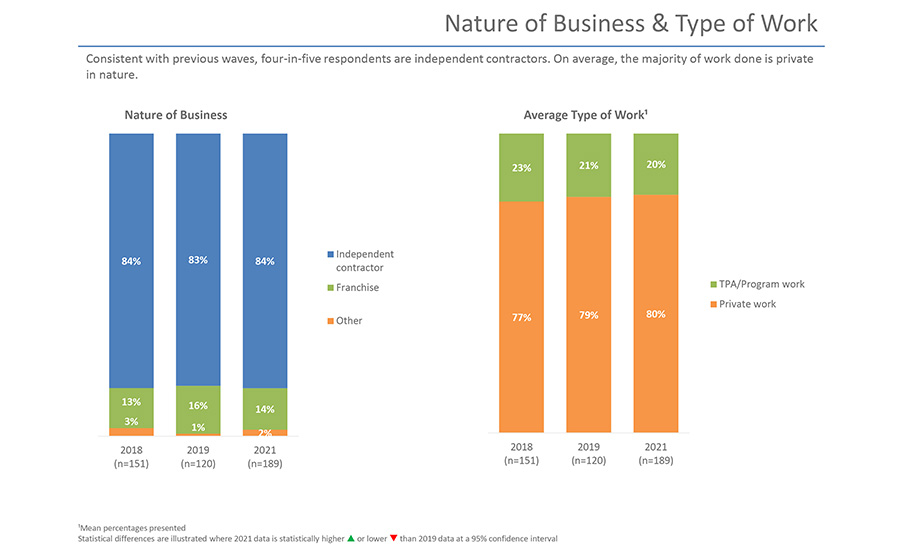

Much of the basic information gleaned from the study remained relatively unchanged from past studies in 2018 and 2019. Eighty-four percent of those who responded are independent contractors; while 14% are franchisees. It’s unclear what that remaining 2% do, but they chose “other.”

Just as in 2018 and 2019, residential work comprised 62% of the workload of respondents in 2021; 28% was commercial; the final 10% industrial.

Click on any image to enlarge

Biggest Challenges

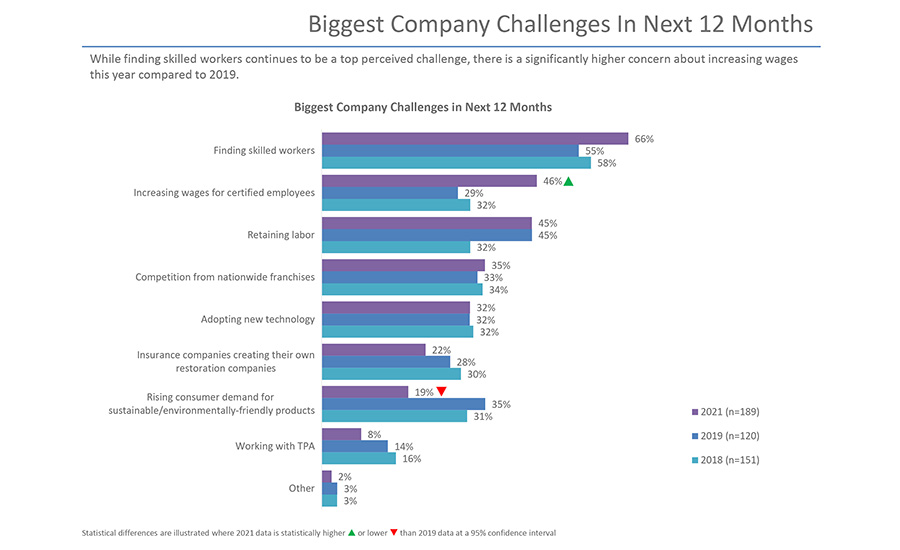

In April, R&R had the privilege of leading a panel discussion at The Experience Conference & Exhibition. While the topic of the panel was lessons from COVID-19, we started the session by using technology to engage with and poll the audience. When we asked about the biggest challenge facing their restoration or cleaning company today, more than two-thirds said hiring and finding employees.

Our State of the Industry study aligned with those poll results perfectly, with 66% saying “finding skilled workers” remains the biggest challenge. Retaining labor was also high, at 45%. Two years in a row, Phil Rosebrook has written about this trend continuing.

“I have worked with several great companies in the past year that have had to limit their growth due to a lack of good people to fill open roles,” wrote Rosebrook in an R&R article in early 2020. “This is a function of a national unemployment rate of near 3.5% and much lower in many areas. With the overall lack of available workers, it is essential that your business has a plan to both find new staff and to retain your current workforce.”

Looking for quick answers on restoration, remediation and cleaning topics?

Try Ask R&R, our new smart AI search tool.

Ask R&R →

In his predictions for 2021, Rosebrook offered this advice as the hiring squeeze continues: “When looking for new staff, you will have to find them where they are currently working. Your job will be to convince them that they have a better opportunity in your business and in our industry. I am always skeptical of people that are out of work right now but you may find people that are not working due to the reality of a post-COVID world.”

Along the lines of hiring, there was a big jump in companies concerned about increasing wages. In 2019, 29% believed wages were a big issue. In 2021, that number jumped to 46%.

There were also significantly more companies reporting a decrease in the size of their staff compared to 2019. Based on job openings and struggles to find employees, this decrease is likely due to inability to find skilled employees.

COVID-19 Impact

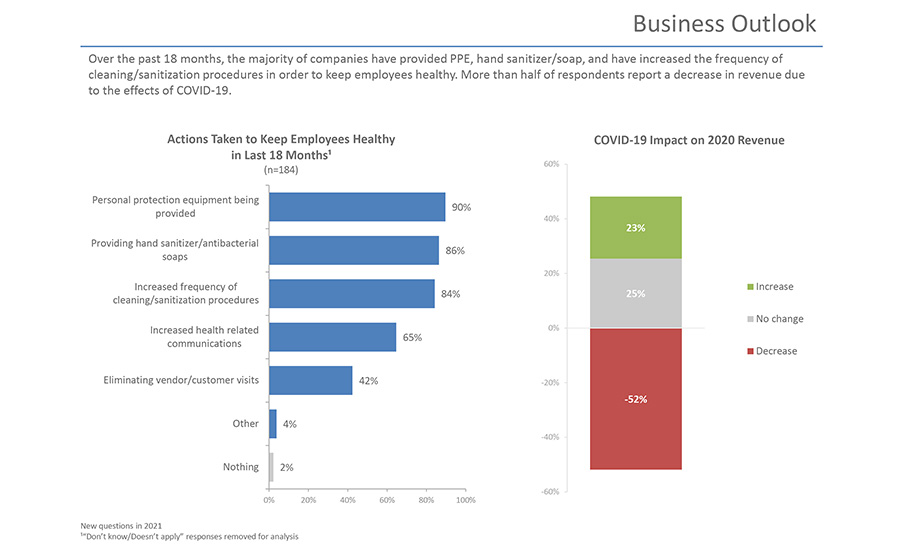

This year, we took some time to try to understand the impact the COVID-19 pandemic had on restoration companies. It does appear the pandemic had a big impact on revenue. Over the past 18 months, more than half of contractors reported a decrease in revenue. Just 23% saw an increase. The good news, as you’ll read later in this article, is most contractors expect to rebound from that well this year.

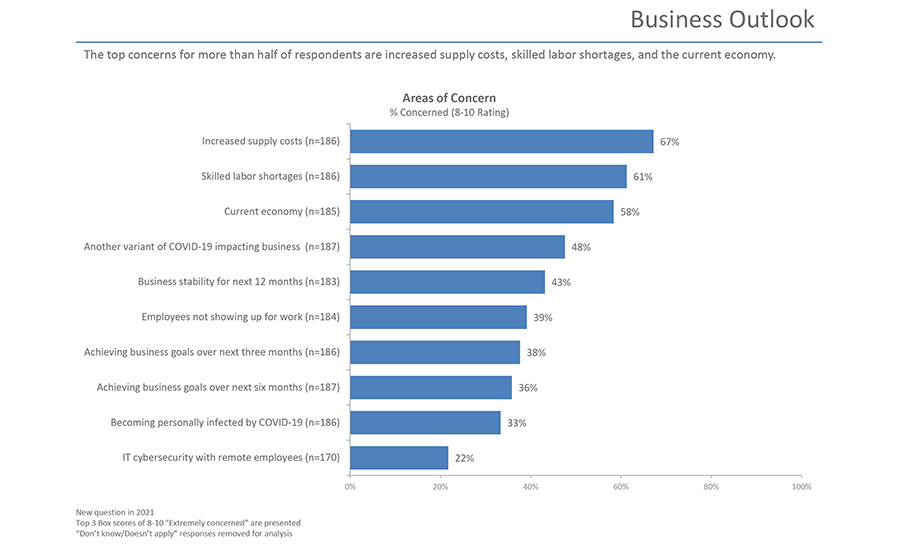

The top concerns for more than half of those surveyed were increased supply costs, skilled labor shortages, and the current economy.

Les Cunningham issued a valuable warning as business trends back toward “normal.”

“Companies seem to relax as they grow older and begin to lose profitability by not holding people accountable for the work that the company needs done at a consistent profit level. As a result, profitability begins to decrease at a time when both the company and the employees want increased compensation and perks,” he wrote in July. His advice is to make sure you, your company, and your team have a solid plan moving forward to be profitable and successful.

Third Party Administrators

This fun topic came up throughout the survey, and overall indicated a decline in both participation and struggles.

Overall, the percentage of TPA work done by companies declined by 3%, from 23% in 2018 to 20% in 2021. The remaining work was private, not provided by a third party administrator.

While we don’t have clear data to concretely identify the small shift, we can draw some educated hypotheses.

First, consultants in the restoration industry have recommended keeping TPA work to 20% or less of a company’s total revenue, so this latest study does indicate the industry trending in that direction.

Secondly, the Restoration Industry Association’s Advocacy and Government Affairs Committee has worked tirelessly to level the playing field between TPAs and restorers. Last fall, they created a TPA scorecard, which will be updated again this year, giving contractors the chance to grade TPAs on a number of factors. There is evidence TPAs have taken those scores seriously, and have worked to implement some changes – although more work is still needed. In 2018, 16% of respondents identified TPAs as one of their major challenges. This year, that number was cut in half, to 8%.

Third, the trend of industry consolidation is also creating new or more innovative network opportunities for contractors.

In summer of 2020, Dan Cassara, CEO of Core Group, talked about the place he sees for contractor networks in today’s restoration industry, and made a good observation about the role TPAs play.

“TPAs, as they were designed, serve a purpose, and that purpose is not exactly the contractor,” Cassara said. “Someone has to be honest about what is really going on – and it is that these systems are not designed for contractors, but they don’t have to be that way.”

He continued by pointing out that contractors often want to point fingers and blame TPAs, but “contractors are the reason these systems were created in the first place. Someone had to hold us accountable. Unfortunately, the good contractors are now left with this thing we built.”

It is from the understanding that TPAs were not built for contractors, and there is work to be done, that groups like Core were formed. Dozens of companies are joining more innovating managed repair networks every month. Plus, groups like Restoration Affiliates, which are equal partnerships among their members, are growing like crazy. Also a major supporter of the RIA’s AGA, member companies of Restoration Affiliates did a combined $693 million in projects in 2020.

Spending Habits & Future Predictions

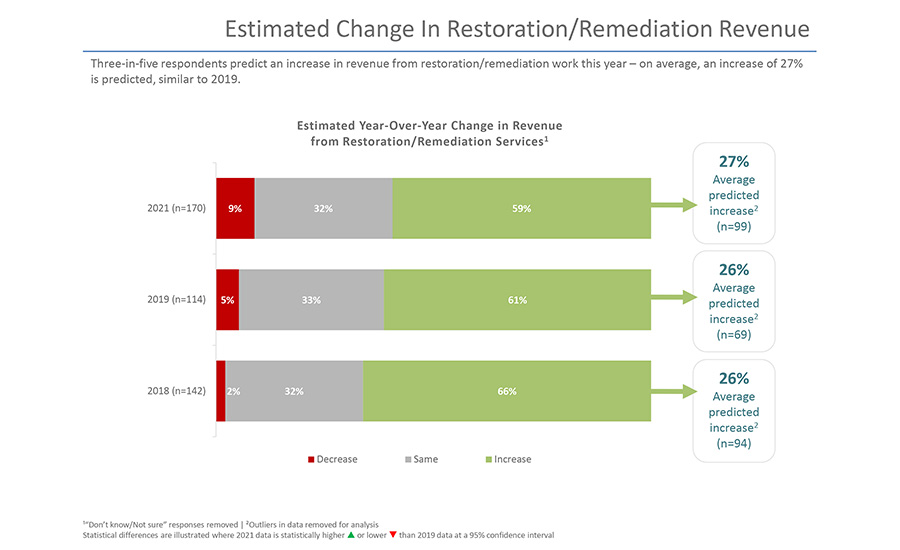

This year, three out of five contractors predict a 27% increase in restoration and remediation work this year, up 1% from years prior, but 9% predict a decrease. That’s up from just 2% in 2018 and 5% in 2019. More work means more purchases.

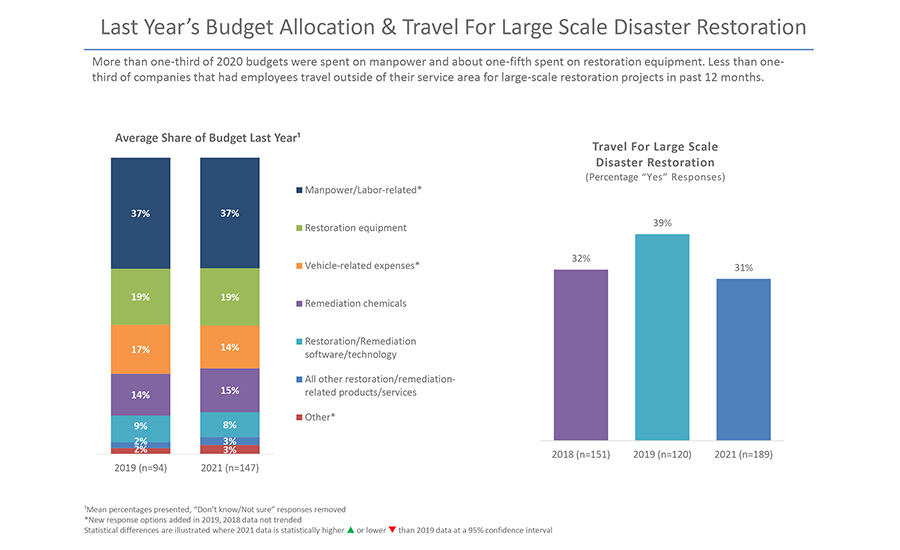

More than 95% of respondents were in a position to affect purchasing decisions within their company, and the share of where the money goes was completely unchanged from 2019 to 2021. More than one-third of spending goes to labor and employees, which we will touch on in the next section.

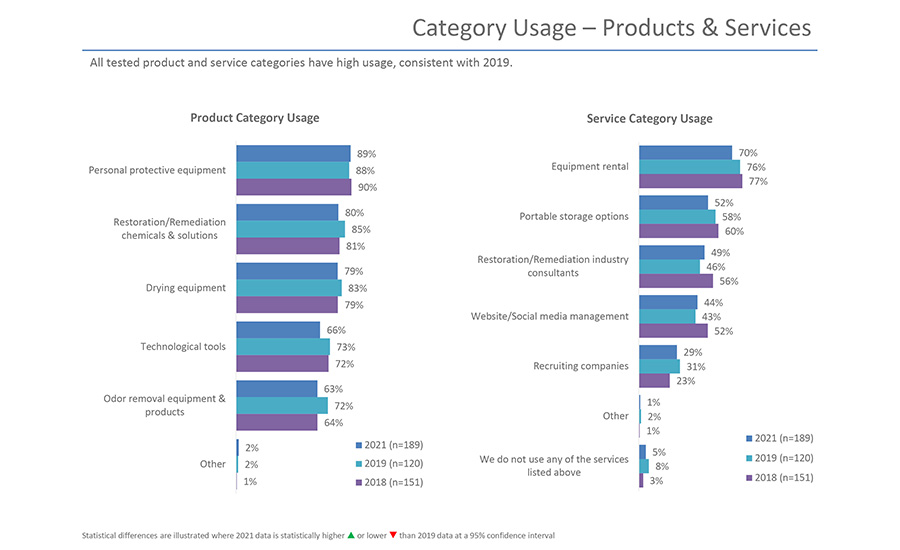

Overall, equipment, product, and chemical usage also stayed virtually the same, with PPE at the top. There was no increase in PPE usage due to the pandemic compared to previous years at all.

The one and only product that saw a noticeable change in usage were thermal imaging/IR cameras. In 2019, 53% of respondents reported using them for restoration companies. In 2021, that fell to 38%.

Conclusion

While this article is just a snapshot of the data captured in R&R’s 2021 State of the Industry study, the trends largely continue to be the same.

A few predictions for years to come: labor shortages continue, the increased use of AI will affect some positions in the restoration industry but not eliminate in-the-field estimators like some have predicted, and of course, consolidation will continue.

Share your predictions with us, so we can take them into account for future articles and content! Email: kingv@bnpmedia.com.

To purchase a full version of this report, visit: https://clearseasresearch.com/product/2021-restoration-remediation-state-of-the-industy/

Looking for a reprint of this article?

From high-res PDFs to custom plaques, order your copy today!

-1.gif")