Insuring Your Risk in Master Service Agreements

*Aaron Millonzi was also a contributing author on this article.

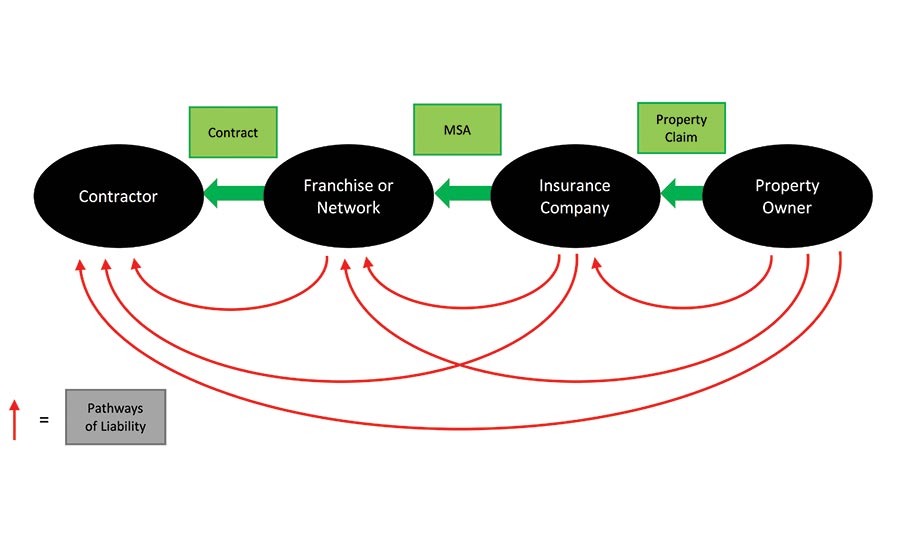

I was recently chatting with a restorer and trying to explain why his insurance needed to be customized to cover the risks he faced in doing work assigned under master services agreements. Upon my second failed attempt to do so, I came to realization this was a complicated subject and that what I really needed was visuals to show how the liability flows between the restorer, the holder of the master services agreement, and the property insurance company.

Here is how liability flows on a job gone bad under a mater services agreement. Note that none of the arrows point away from the restorer.

In a nutshell, the restoration firm will always be responsible to pay for any damages caused by its operations or completed operations at the job site. In addition, the restorer will pay for losses his work caused to other parties in the chain. The only question is who will the restorer have to pay on a job gone bad; it could be the property owner, the holder of the master services agreement, or the property owner’s insurance company. Because of the indemnity agreements in the master services agreements, the restorer will also end up paying for any costs incurred to pay lawyers to defend any indemnified parties in the master services agreement contract.

The grantors of master services agreements, and the direct repair networks and franchise operations that arrange for the work to be done under those contracts, all know that the restorer is responsible under the contract for all the costs incurred by all of the parties. They also know that they want the restorers to be insured for any damages the restorer may cause. If there is a coverage gap in the liability insurance coverage, the restorer will be the insurance company of last resort for all of the parties the restorer has indemnified.

The most common coverage flaw that we find in the insurance policies sold to restorers working under master service agreements is with the Additional Insured (AI) endorsements. An Additional Insured (AI) endorsement amends the definition of who is an insured under the insurance policy.

Here is some self-help information:

- If your Additional Endorsements do not specifically say that the holder of a master services agreement is an Additional Insured on your General Liability and Contractors Pollution liability insurance policies, the parties you agreed to indemnify (pay for losses they may incur because of your operations) will not have the benefit of your insurance coverage. Without insurance to back you, you will become the deep pocket that everyone will look to for payment of their losses. There is an exception to this general rule, some blanket additional insured endorsements work on the combined GL/CPL policies.

- Another self-help tip is if you have separate General Liability and CPL policies in different insurance companies — you are likely in trouble on the needed Additional Insured coverage for jobs assigned to you under master services agreement contracts.

A Real-World Case Study

To help you understand why it’s so important to have proper AI endorsements for dealing with master services agreement, let’s walk through a real-life claims example that I experienced with one of my own restoration contractor insurance buyers.

Looking for quick answers on restoration, remediation and cleaning topics?

Try Ask R&R, our new smart AI search tool.

Ask R&R →

The claim started as a standard drying job in a home. The second-story bathroom tub had been leaking, causing water damage. My restoration contractor client was called in to deal with the water damage. It was discovered that the cause of the leak was a broken tub drain, so a plumber was dispatched to repair that. Since the bathroom was on the second story, the easiest way to access the drain was from the first story up, through the ceiling. Unbeknownst to the plumber and my client, the bathroom was originally a second story front porch, and drywall had been put over the exterior asbestos tiles in the remodeling process. So, when the plumber — who did not carry Contractors Pollution Liability (CPL) insurance — fired up the saw and started cutting through the ceiling tile, he ended up releasing asbestos dust. This dust was quickly circulated throughout the home courtesy of the drying fans being run to mitigate the water damage.

Suddenly, a $5,000 drying job had turned into a $40,000 asbestos abatement arising from a leaking drain that the homeowner’s insurance policy was going to pay for, or at least initially pay for.

As could be expected, asbestos dust in the house resulted in an upset homeowner who wasn’t shy about sharing his frustrations with his homeowner’s insurance company paying for the leaky drain loss. The homeowner’s insurance company had a master services agreement in place with the franchisor of my restorer customer. Very quickly the franchisor was notified that it owed the insurance company $35,000 for the extra cost of an asbestos abatement in the home. Within hours, the franchisor was in pursuit of the franchisee for reimbursement of the $35,000.

Within a few days, the homeowner became evermore distraught upon the discovery of asbestos fibers on his infant’s clothing. His reaction to this news was to have the entire home bulldozed. From a simple $5,000 drying job to a $40,000 asbestos remediation (which never happened) culminated in a complete demolition and rebuild of the home costing over $900,000.

The entire $900,000 loss was set off in sequence from the leaking drain, which was a covered loss on the homeowner’s insurance policy. The homeowner’s insurance company carrier quickly turned to the franchisor for indemnification via the master services agreement for the entire loss minus the $5,000 drying job. Fortunately, we had the proper coverage in place, and the entire loss was covered and paid for by my contractor’s liability insurance company.

Standard Contracts

Here is a refresher on what a contractor commonly agrees to in a standard contract with a franchise organization or a direct-repair network. In these franchise agreements or network procurement contracts, the contractor agrees to pay for all costs the franchisor or the network incurs as a result of a claim coming from the contractor’s job site. A claim can come from a handful of sources and find its way to the contractor in a few different ways:

- A claim may be brought directly from the property owner to the contractor. There is no Additional Insured needs in that claims scenario.

- It could filter through from the property owner to their insurance company back to the contractor because the insurance company now has to pay more for a property loss based on something the contractor did.

- It might make its way from the property owner to the franchisor or network and to the property owner’s insurance company to the contractor.

In that real-world example earlier, the claims process followed a neat path of liability from the insurance company to the holder of the master services agreement back to the contractor. It might not always follow this same pattern. As I noted before, the claim can reach the contractor through various avenues. Sometimes the homeowner brings a suit against all the parties involved: the contractor, the franchisor or the network, and the homeowner’s insurance company. When that happens, having all of the parties that were indemnified by the restorer in the master services agreement insured under the liability insurance policies of the restoration firm is really important.

Here is an actual example of how one of these multi-party claims gets set in motion.

Dear Master Services Contract Holder:

This letter is to inform you that INSURANCE COMPANY is putting you on notice that we may be pursuing you for costs associated with unnecessary delays including delays related to correcting construction deficiencies for work performed by your vendor, CONTRACTOR. These costs could include, but not be limited to, engineering fees, additional living expenses, as well as increased construction costs associated with correcting current construction deficiencies.

What if in addition to the above demands the homeowner was alleging, their children could not learn in school anymore due to mold in the home which was caused by the project delays caused jointly by the insurance company, the master services agreement holder, and the contractor? That is when having the Additional Insured coverage for the homeowner’s insurance company and the holder of the master services agreements is critically important. In that example, the contractor’s liability insurance policy will need to pay for the defense costs of each indemnified party.

Not having the proper insurance doesn’t negate the contractor’s indemnity responsibility. It simply means the contractor will pay all of these costs out of pocket.

The good news is that the extension of insurance coverage to the AI is almost always free of charge if the coverage is requested at the time the policy is purchased. The bad news is the coverage for the AI hardly ever works for master services agreements in off-the-shelf insurance contracts.

A Fatal Flaw

The fatal flaw in the insurance sold to the vast majority of restorers is this: For an entity to enjoy the benefits of being an Additional Insured on the liability insurance policies of a contractor, the insured contractor must be performing operations for the entity that expects to be an AI at the address of the Additional Insured party. That scenario never happens. The jobs performed under a master services agreement are never performed for the holder of the agreement. The work is performed under direct contract with the property owner. Therefore, none of the criteria for being an Additional Insured are met.

The good news is there is a solution to this Additional Insured predicament associated with direct-repair networks and any party holding a master services agreement for restoration services with an insurance company. The important thing is to not make the AI status dependent upon working for or at the location of the AI. Some customized combined GL+CPL policies and CPL policies designed for restoration firms have this coverage built in. However, that is rarely the case on General Liability insurance policies.

A simple check you can do on your own is to pull out your policy and see if it has both CG 20 10 and CG 20 37 Additional Insured endorsements on the General Liability policy. If you are performing services for the holder of a master services agreement with an insurance company and you don’t have CG 20 10 and CG 20 30 on the General Liability insurance policy naming the appropriate parties as Additional Insureds, that is a red flag.

If you’re concerned that your insurance program might have the very common Additional Insured coverage gaps discussed above, give us a call with your liability insurance policy in front of you! We can sort through it all with you usually in a matter of minutes, and figure out if you are covered or not. We do not charge for this advice.

Looking for a reprint of this article?

From high-res PDFs to custom plaques, order your copy today!