To Get Top Dollar, Look Beyond the Numbers

Working with cleaning and remediation companies throughout the U.S and Canada, I have two crystal clear observations. First, it’s obvious which owners have prepared to sell their company, and which have not. Second, all owners (prepared or not) desire top dollar for their firms. Can their companies be sold for the highest price? Absolutely. But here’s the secret: some top dollars are much better than others.

I’m not talking about a larger company selling for $15 million and a smaller one for a fraction of that amount. I am referring to securing a ‘premium value’ for your business versus accepting an offer that is 5% to 30% less. It’s simple: all businesses are not created equal. How can you tell the difference? You must look beyond sales, profitability or earnings.

Using GAAP Methods to Value Your Company

Let’s compare Company ‘A’ and Company ‘B.’ Comparable in total sales, employee structure, number of vehicles, and amount of assets, they appear to be similar. After applying four GAAP (Generally Accepted Accounting Principles) business valuation methods to the two companies, each is valued at $1.5 million for a standard investment-type buyer.Here is the ultimate valuation lesson. These four GAAP valuation methods use numbers only derived from balance sheets, tax returns, and profit and loss statements. They do not incorporate any other variables that could add to or detract from the value established through the valuation methods. Using only numbers, any other variable associated with a business (and not found in the numbers) is not considered part of a basic valuation and therefore omitted. So based solely on the numbers, these hypothetical companies are both valued at $1.5 million.

Do you see the problem? This is not reality. There are always dozens of variables found in businesses that impact the price in either direction. Why? These variables are perceived as either adding or reducing risk.

No. 1: Timing

There are three main variables when considering timing: Are you ready? Is the business ready? Is the market ready?Rarely do all three align perfectly. The cleaning and remediation has proven recession-resistant not recession-proof as many thought. With the market not providing any favors the last three years, a seller can hope for the best possible alignment of being ready personally, along with the business being ready. With these two in harmony, excellent prices are still attainable.

No. 2: Financial Trend

Are the Gross Sales, Net Profit and Adjusted Earnings (or EBITDA) figures trending upward or downward?Trending upward is always better, adding value by adding confidence. As it has been said, “Selling a business is a bit like selling a stock. When it’s hot, it’s much easier to sell.”

No. 3: Owner Involvement

Is the owner working 15-20 hours, or 70-80 hours, per week?Two of the buyer’s initial questions are always “What does the seller do?” and “Can I replace him/her?” Working less is always better than working more. Psychologically, the seller becomes easier to replace.

No. 4: Management Quality

How capable are key employees? And, how long have they been with the company? Long-standing employees have a better understanding of the business and its processes. This alleviates some risk in the buyer’s mind.No. 5: Client Risk Factors

Does one insurance company or TPA (Third-Party Administrator) account for more than 25% to 30% of total sales?A buyer will raise a red flag any time one company or a TPA accounts for more than 25% to 30% gross sales. More importantly, they’ll look at how many insurance agents or adjusters refer work from those companies. An insurance company accounting for 30% of Gross Sales is far less risky if there are six to seven adjusters referring work, as opposed to just one or two.

No. 6: Asset Quality

The significant asset category is typically the vehicle fleet. What is the average age and condition of the fleet?Buyers will be on high alert for an older or aged fleet with deferred maintenance. Try to keep the average age of the fleet below 5-7 years. Newer is always better than older, eliminating the buyer’s need for immediate capital investment.

No. 7: Professionalism

Generally, are there systems and procedures in place for many or most of the operations of the business?This category can also reach into issues such as employee turnover, focus on safety/education, and level of workers compensation claims, employee manuals, litigation history, etc. Simply, when owners keep their processes and information undocumented (in their head), it is riskier than a company with a base level of written systems and operational procedures.

No. 8: Reputation / History

Does the company have a strong reputation with solid referral sources?As most are fully aware, this industry is built on relationships. Many times the strength of those relationships is a direct reflection of a company’s reputation, and vice versa.

No. 9: Financial Cleanliness

Financial documents can be described as ‘clean’ or dirty.’ Is there a clean paper trail for adjusted earnings (total financial benefit to the owners), allowing a potential buyer to clearly see how money flows out of the company?Buyer and lenders alike are able to build confidence with ‘clean’ financial statements. When too many shell games are played with money, uncertainty surrounds the financial statements and confidence dwindles.

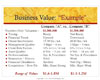

Chart 1

No. 10: Competition

There will always be competition. However, are there solid communication and relationships in place with other local cleaning or remediation companies? And, is there a sustainable market share that can be grown?Buyers want to know how a company ‘fits’ into the market place. In addition, they’ll look for referral relationships with vendors and subcontractors, as well as the presence of any market niches or specialties allowing them to compete successfully at the highest possible margins.

Which Company is Worth More?

Back to our examples of Company ‘A’ and Company ‘B,’ let’s compare the two businesses again (Chart I). The variables are not found on a balance sheet, tax return or P&L, but they are obviously capable of affecting value:What’s the final result? Company ‘A’ is prepared! It is no longer worth $1.5 million. The new transaction value is between $1.6 million and $1.8 million, an increase of 5% to 20%! Unfortunately, with several risky issues to overcome, Company ‘B’ is ill prepared. The new Transaction Value is between $1.1 million and $1.3 million, a significant decrease!

In this typical example, a value difference of $400,000 to $500,000 is both possible and realistic. To those with larger companies, the value difference can be in the millions of dollars. It’s absolutely critical for company owners to understand these are real dollars to be gained or lost at the point of a transition.

At some point a buyer will be asking, “How does each of these variables affect the value of the company?” You owe it to yourself to be asking the same questions well in advance.

Looking for a reprint of this article?

From high-res PDFs to custom plaques, order your copy today!